When A Citizen Spouse Passes But the HDB Is In Both Names - Must You Sell?

In this article, I wanted to walk through a scenario that’s more common than people admit, but rarely talked about openly.

It’s about grief, "stringent" housing rules, and a very specific kind of anxiety:

“My spouse has passed away. I’m a PR co-owner of an old HDB. Do I have to sell, and if I do, what happens next?”

Let’s call our case study Madam L.

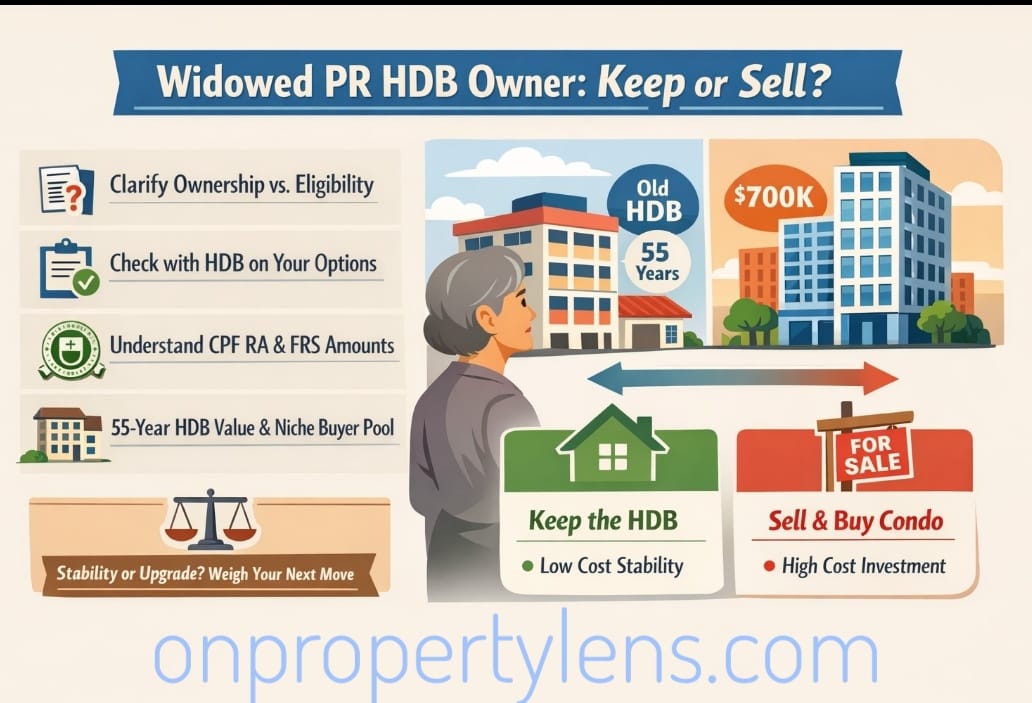

The Case: 60-Year-Old PR Widow, 55-Year-Old HDB

Madam L is 60. She’s a Singapore Permanent Resident and was married to a Singapore Citizen for more than 30 years.

Background Key facts:

They own a 3-room HDB flat, about 55 years old

The flat is fully paid off, bought mainly using her CPF

It’s held in both their names under the Joint-tenancy.

Their children are grown, married, and living overseas. They are not Singaporeans or PRs

Recently, her husband passed away.

On top of coping with grief, she starts hearing “advice”: (well-meaning friends & relatives)

“Your flat is so old, better sell before it becomes worthless.” (effect of lease decay)

“You’re a PR, no more citizen family nucleus – HDB will force you to sell.” (Subject to HDB's Eligibility and Conditions)

“Sell now, use the money and your $700K budget to buy a freehold condo. Better investment.” (Looking out for next upcoming article -Buy Freehold or Leasehold Better)

Emotionally, she wants to stay in the flat where she spent decades with her husband. Rationally, she worries: what if HDB really forces me to sell?

If you’re

a widowed/older HDB owner, a PR married to a citizen, or an investor with ageing HDB exposure, this is the kind of situation worth understanding before you’re in it.

Step 1: Ownership vs Eligibility – Two Different Questions

When a spouse passes away, most people think in very simple terms:

“The flat is in both our names. Now that he’s gone, it’s automatically mine, right?”

Partially true, but incomplete.

Two separate “filters” apply:

Legal ownership (property law / succession)

HDB eligibility (who is allowed to own an HDB)

Don't be surprised that most Singaporeans/PRs are not aware: You need both to go in your favor.

1.1 What happens to the flat when one owner dies?

Most married couples hold their HDB as joint tenants.

Under joint tenancy, there is a “right of survivorship”:

if one owner passes away, the other automatically becomes entitled to the entire property.

In practice, the surviving spouse (like Madam L) needs to:

Lodge a Notice of Death with the Singapore Land Authority (SLA)

Get HDB / the lawyer to update the title so she is now reflected as the sole owner. Make appointment with the HDB branch and not at the HDB Head Office at Toa Payoh.

So from a legal title point of view, it’s actually quite straightforward:

Yes, madam L can end up as the sole legal owner of the flat.

1.2 But HDB then asks: are you allowed to keep it?

This is where it gets tricky.

HDB doesn’t just look at the legal title. It also applies ownership eligibility rules. And for PRs, those rules are quite specific:

A single PR generally cannot buy or own an HDB flat on their own

PRs usually need a family nucleus with a Singapore Citizen or PR spouse/children/parents etc.

Before her husband passed, the “family nucleus” was clear: Citizen + PR.

Now, due to life events, there is a change in status - Madam L becomes a PR widow with no Citizen children in Singapore.

From HDB’s perspective, a few outcomes are possible, typically on a case-by-case basis:

Allow her to retain the flat on compassionate grounds

Allow retention, but with conditions

Or require her to sell the flat within a specified period

Notice the nuance:

There is no simple public rule that says, “All PR widows must sell.” which I don't think anyone can find the rule on the HDB official web site.

1.3 Practical steps right after a spouse’s passing

If you’re in a similar situation, here’s a practical to-do list:

a. Confirm how the flat is held

Check: joint tenancy or tenancy-in-common

b. Update the ownership record

d. Write formally to HDB to explain your situation: Explain your situation: age, PR/citizen status, children’s status, income, health, that this is your only home

2. Appeal if needed

If your case is borderline, seek help through your MP and formally request to retain the flat.

Before (A critical one) you start viewing private condos or worrying about “investment potential”, this is the first question to resolve:

“Can I keep my HDB at all, and if yes, under what conditions?”

Step 2: If You Must Sell – What Is a 55-Year-Old 3-Room Really Worth?

Let’s assume the outcome is:

HDB allows you to keep the flat → then selling is a choice, not a legal requirement.

HDB requires you to sell → you now need a realistic plan.

For a 55-year-old 3-room flat in a mature estate, here’s the broad reality.

2.1 A realistic value band

Recent resale data for 3-room flats in the 54–56-year age range (older, established estates like Toa Payoh, Queenstown, Bukit Ho Swee, Old Airport) shows most transactions roughly in the:

Mid-$300,000s to Low-$400,000s

The exact price depends on:

Block and street

Storey height

Interior condition

Distance to MRT, amenities, etc.

So, for someone like Madam L, it’s not crazy to assume her unit might fall somewhere in the $350K–$420K range.

(Not a valuation, just a working assumption.)

2.2 Where we are in the price cycle

Across almost all age groups, 3-room HDB prices surged after 2020. Covid, BTO delays, and housing demand all contributed.

But if you look over a longer horizon:

Newer flats tend to see stronger sustained growth

Very old flats (1960s–1970s) did rise, but their growth has been more muted and volatile, reflecting concerns about lease decay and tightening financing rules for short leases

The takeaway for an owner of a 55-year-old flat:

You’re probably selling into a relatively strong price environment, but you still face structural limits because of the short lease.

2.3 Why old 3-rooms aren’t as easy to sell as people assume

The flat’s age affects your buyer’s financing:

Banks may reduce the loan-to-value for very old flats

CPF usage is curtailed if the buyer’s age + the remaining lease doesn’t hit certain thresholds

Some grants may be reduced or unavailable for older flats

End result: your buyer pool shrinks.

Likely buyers are:

Older couples right-sizing

Singles

Niche buyers who really want that location and accept the short lease

So yes, you may get a fair price. But you are not selling a 10-year-old flat in Punggol or Tampines with a long queue of young families.

Step 3: What Happens to Your CPF If You Sell in Your 60s?

This is the piece many older owners overlook.

3.1 The CPF refund rule

When you sell, any CPF you used for the flat – plus accrued interest – must be refunded to your CPF accounts.

For those 55 and above, the refund doesn’t just sit in OA:

It first goes to your Retirement Account (RA)

Up to your cohort’s Full Retirement Sum (FRS)

Only any excess goes into your Ordinary Account (OA)

3.2 What this means for Madam L

Madam L is 60 in 2025, which means she turned 55 in 2020.

For the 2020 cohort, the FRS is $181,000. (Full Retirement Sum)

So:

If the CPF refund on sale is less than $181K, almost all of it may end up in her RA (for retirement payouts), not in OA

Only when the RA hits $181K does any extra go into OA for a new property

For those who're below 55 - The entire refund goes into your Ordinary Account (OA). You can then use it for various CPF schemes, including purchasing your next property, or transfer it to your Special Account (SA) for higher interest and retirement payouts.

This is why “I’ll sell for $380K–$400K and use it all for a condo” is usually not how the numbers play out.

Between transaction costs and the CPF refund sequence, the usable amount for the next purchase is often much lower than the headline selling price.

3.3 What you should do before even looking at condos

If you’re in your late 50s or 60s and thinking of selling:

Log in to CPF

- Check:

How much CPF was used for the current flat (plus interest)

Your RA balance

How far you are from your FRS

- Ask:

If I sold today, how much would be refunded?

How much would go into RA vs end up in OA?

Without those numbers, any talk of “$700K budget” is just an estimate, not a plan.

Message me to get detailed calculation to your specific situation.

The Upgrade Idea

Step 4: Can a $700K Freehold / 999-Year Condo Work – and Should It?

Let’s directly address the upgrade idea.

4.1 What $700K usually buys in freehold/999-year

Sub-$700K freehold or 999-year units in today’s market are typically:

Studios or compact one-bedders

Around 350–450 sq ft

- In city-fringe or fringe areas like:

Parts of Geylang / Paya Lebar / Sims

Some Eunos / Kembangan / Kovan / Upper Serangoon pockets

Often in smaller boutique projects rather than large full-facility condos

So yes, at face value, a $700K freehold shoebox is not a fantasy.

But for a 60-year-old widow with no active income, the more important question is: is it wise?

4.2 Trade-offs for someone like Madam L

Here’s what she would be exchanging:

From:

A fully paid-up HDB

Low, predictable monthly S&CC

Reasonable living space (3-room layout)

Long-established neighbourhood and support network

To:

A small 350–450 sq ft unit

Significantly higher monthly maintenance fees

Potentially higher property tax

More volatile valuations (private market)

A concentrated bet on a single asset

On top of that, as a PR, if she buys a private residential property, she generally needs to sell her HDB within 6 months plus a 5% stamp duty.

There is no “test drive the condo and move back if I don’t like it” option.

Same HDB Flat, same life events (widow)

But..

For an investor in their 30s or 40s with stable income, this may be a reasonable move.

For a 60-year-old widow with no income, the risk profile is very different.

There is also another quite common question to ask:

"Will I be "subsiding" my younger condo neighbors in paying the Quarterly maintenance fees who are likely to use the condo/apartment facilities more frequently compared to me)?

For buyers who are looking at condo, one of the good question to ask: Am I buying condo because of the condo facilities/lifestyle? If yes, you have more reasons to purchase.

Step 5: A Simple Framework –

Stay vs Sell

Once HDB has told you whether you can keep the flat:

Scenario 1 -

HDB allows you to retain the flat

Strong reasons to consider staying put:

The flat is fully paid – your main housing cost is S&CC, not mortgage + maintenance

You value stability more than potential capital gains

Your health, mobility, or social network makes moving more of a cost than a benefit

- Your retirement risk is better managed by:

Low fixed housing expenses

Possibly tapping Lease Buyback later (if eligible)

Renting out a room if you’re comfortable and allowed

In many cases, a paid-up HDB flat is a very strong retirement asset – not because it will make you rich, but because it reduces the risk of you ever being forced to sell again.

Scenario 2 - If you must sell or strongly want to upgrade

Then, before you touch a condo showroom:

Clarify your true net proceeds

Understand your CPF flow (how much goes to RA vs OA)

Stress-test your monthly cashflow with higher maintenance and tax

Ask:

“If my investments disappoint and my kids can’t support me as much as I hope, can I still comfortably hold this condo for 10–20 years?”If that answer makes you uneasy, it’s a signal to rethink.

Closing Thought – The Real Question Isn’t “HDB vs Freehold”

For someone like Madam L, the real questions are:

Can I keep my HDB as a PR widow, and if so, under what conditions?

If I sell, how much am I really left with, after CPF and retirement sums?

Does moving to a small freehold unit actually improve my long-term security, or just change my postal code?

If you or someone you know is in a similar position and want help thinking through the numbers and scenarios, hit reply and share (even broadly) what you’re facing. I can’t give individual financial advice, but I can help you structure the decision so it’s driven by facts and cashflows, not fear and rumors.

P.S. If you’d find it useful, I’m thinking of putting together a one-page checklist: “What to do with your HDB if your spouse passes on and you’re a PR/older owner.” Reply with “HDB checklist"” if you’d like that and I’ll prioritize it.